📰 THIS WEEK’S HEADLINES

SPONSORED BY

📰 THE LENDER DRAFT WEEK’S RECAP

Forget everything you thought you knew about this bracket. While the #1 seeds were busy warming the bench, the Cinderellas crashed the party. Second Avenue Capital Partners jumped 20 spots on a single $126M syndication while nFusion Capital climbed 20 spots with one modest $3M Factoring deal. Meanwhile, Wells Fargo—the top-ranked CRE lender—put up a donut. This is March Madness in February, folks.

🔥 TOP PERFORMANCES: WHO PUT ON A CLINIC?

#2 Goldman Sachs 93, #1 Wells Fargo 60 (33-point rout) – CRE

The defending #1 seed got embarrassed at home. Goldman dropped $650M across two deals (including a $596M refinancing for The Crescent towers in Dallas), while Wells sat on zero. Goldman holds #2, Wells clings to #1 by a thread. Next week could flip the script.

#13 Ares Management 91, Stellus Capital 60 (31-point rout) – Growth Capital

Ares just reminded everyone why they’re a problem. One deal. $2.4 BILLION debt facility for Vantage Data Centers. That’s not a typo. While Stellus was MIA, Ares dropped the biggest bomb of the week and jumped 9 spots to #13. When you go big, you go REALLY big.

#1 SouthStar Capital 93, Clarus Capital 70 (23-point win) – ABL

SouthStar is the #1 seed in ABL for a reason. Three small-ticket deals ($750K, $2M, $1.5M) across construction, manufacturing, and tech—pure volume play. They’re now sitting on 8 total deals and 61 cumulative points. The rest of the bracket is chasing.

😱 UPSET OF THE WEEK

#19 Santander 104, #10 Deutsche Bank 70 (34-point demolition) – CRE

The #19 seed just went absolutely filthy on Deutsche. Santander co-originated a $355M solar-plus-storage financing in Chile AND provided €175M for a Portuguese renewable portfolio while the #10 seed didn’t close anything. Santander rocketed up 9 spots to #11.

Check out full scores at https://thelenderdraft.com/march-madness-week-6-feb-2026-scores/

📊 THE LENDER DRAFT STANDINGS SHAKEUP

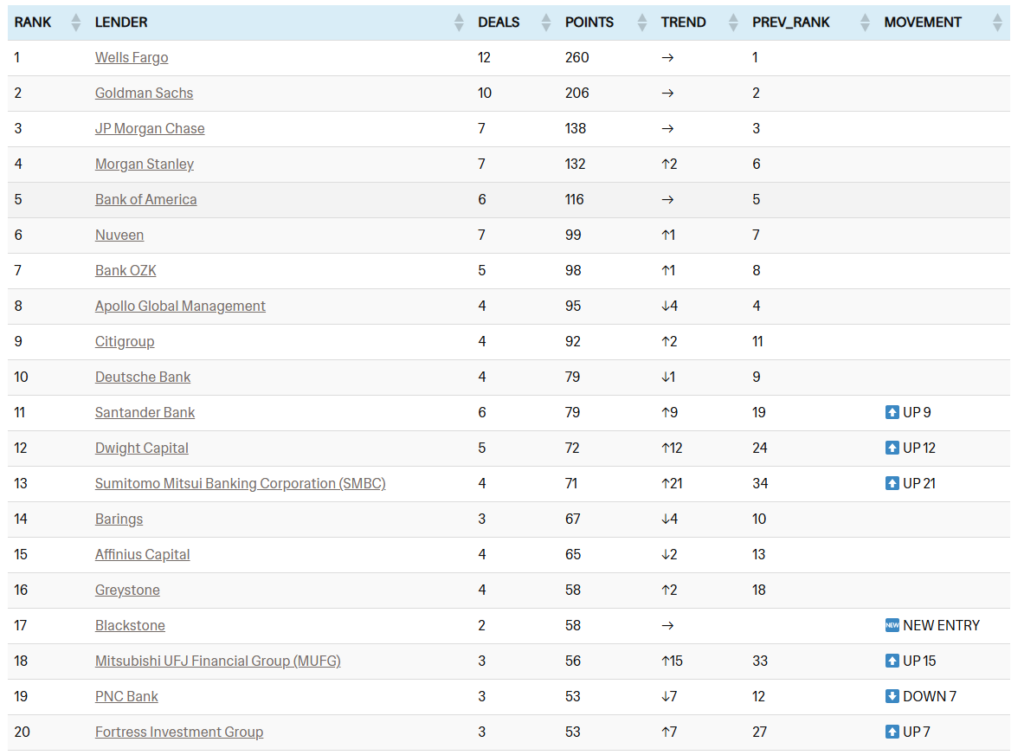

🏠 CRE LEADERBOARD

🔝 THE RISERS:

- #13 SUMITOMO MITSUI (SMBC) ↑21 (U.S.: 4 deals, 71 points | International: $427M deployed)

- #18 MITSUBISHI UFJ (MUFG) ↑15 (U.S.: 3 deals, 56 points | International: $375M India transmission)

- #12 DWIGHT CAPITAL ↑12 (5 deals, 72 points) | HUD-backed construction deals

🆕 NEW ENTRIES: #17 BLACKSTONE, 1 deal International $10 billion Australia AI factory deal

BEST MATCHUP GAME

Madison Realty Capital 79, Affinius Capital 75 (nail-biter)

Talk about a heavyweight slugfest between private credit players. Madison co-originated a $371.5M construction loan for Nashville Edition Hotel & Residences (261 rooms, 64 residences) alongside KSL Capital Partners, while Affinius countered with a $90M refinancing for a luxury Brooklyn multifamily. Both showed up. Madison edged it on volatility and is now positioned at #25—watch this space.

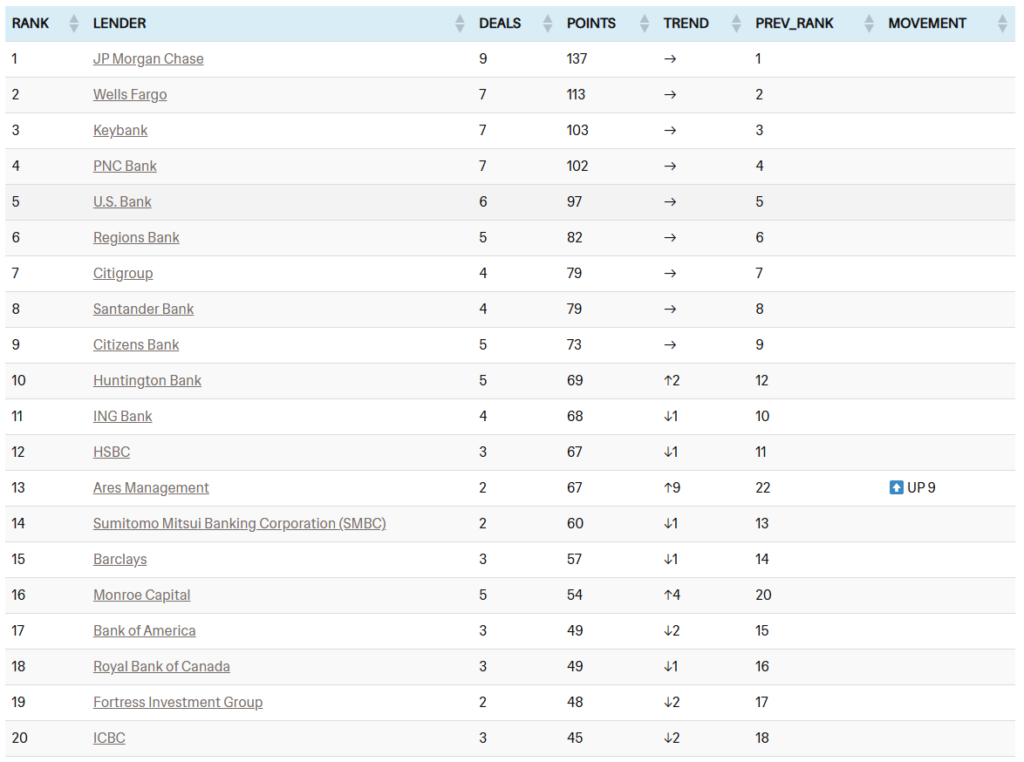

💼 GROWTH CAPITAL LEADERBOARD

🔝 THE MOVERS:

- ARES MANAGEMENT: #13 (↑9) | 2 Deals, 67 Points

- MONROE CAPITAL: #16 (↑4) | 5 Deals, 54 Points

BEST MATCHUP GAME

#30 Leonid Capital Partners 96, Mitsubishi HC Capital 80 (16-point win)

Leonid came to play. Two credit investments—one for Senvias (advanced manufacturing/composite materials) and another for AxNano (PFAS destruction systems). Not the flashiest sectors, but smart capital deployment. Leonid shot up to #30 and is now making noise in the Growth Capital bracket.

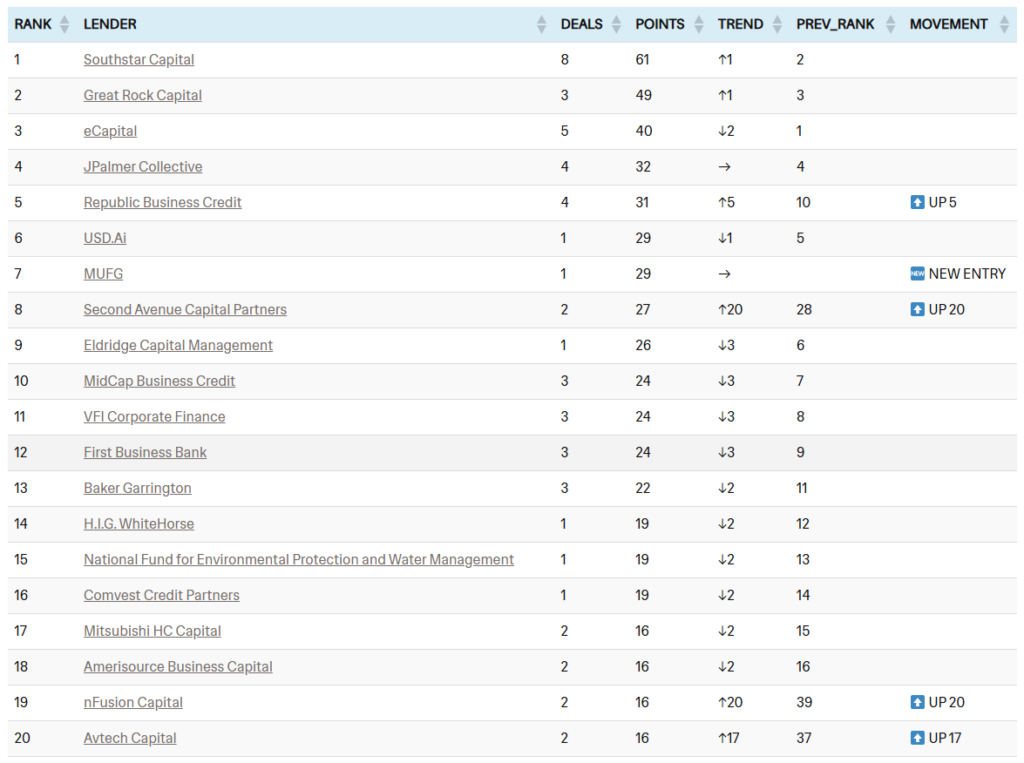

⚡ ABL LEADERBOARD

🏆 THE ELITE:

- SECOND AVENUE CAPITAL PARTNERS: #8 (↑20 – UP TWENTY!)

- nFUSION CAPITAL: #19 (↑20 – UP TWENTY!)

- AVTECH CAPITAL: #20 (↑17 – UP SEVENTEEN!)

🆕 NEW ENTRY: MUFG: #7, 1 deal, 29 points

BEST MATCHUP GAME

Second Avenue Capital Partners 79, Great Rock Capital 75 (4-point thriller)

This was an instant classic. Second Avenue served as Admin Agent on a $126M senior secured credit facility for Mirai Casting Group, while Great Rock lead-arranged a $175M revolver for a crane rental company. Great Rock actually had the bigger deal, but volatility swung it to Second Avenue. Second Avenue vaulted 20 spots from #28 to #8. One mega-deal changes everything in ABL.

🏆 THE LENDER DRAFT LENDERS OF THE WEEK

COMMERCIAL REAL ESTATE

Offensive Lender of the Week: Goldman Sachs

This Week: 3 deals | 63 points

Biggest Deal: $1.47B | CMBS Refi for Ares Industrial Portfolio | Ohio, Tennessee, Indiana, Georgia, Florida

.

Defensive Lender of the Week: Morgan Stanley + Bank of America

The Play: $407M refinancing | 20-year WALT | 100% leased to blue-chip tenants | NYC Class A office

GROWTH CAPITAL

Offensive Lender of the Week: Ares Management

This Week: 1 deals | 36 points

Biggest Deal: $2.4B | Debt Facility for Vantage Data Centers | Denver, CO

Defensive Lender of the Week: Monroe Capital

The Play: $40M senior secured facility + $10M accordion | Israeli medtech | Milestone-based growth optionality

ASSET-BASED LENDING

Offensive Lender of the Week: MUFG

This Week: 1 deal | 29 points

Biggest Deal: $500M | Non-Recourse Turbine Warehouse Facility Secured by Equipment | Amarillo, TX

Defensive Lender of the Week: Republic Business Credit

The Play: $8.5M ABL facility + $1.25M equipment term loan | Covenant package tied to sponsor capital commitments | Midwest transportation

💡 WHAT THIS WEEK TELLS US

1. The “Superteam” Era is Here. Look at the box scores in CRE. Goldman and JPM teaming up on The Crescent ($596M). BofA and Morgan Stanley on Lexington ($407M). Lenders are realizing they can’t win the championship alone. They’re forming superteams to take down massive refinancings. Syndication is the new alley-oop.

2. ABL is all about “Small Ball.” SouthStar proved you don’t need a whale to win the week. A $750K deal counts. A $2M deal counts. In the ABL bracket, speed kills. The lenders who are processing volume are running circles around the guys waiting for the “perfect” deal.

3. For Borrowers: Lenders are accepting “Compute” (GPUs) and “Power” (Turbines/BESS) as senior collateral. If you are a tech company, stop seeking “Venture Debt” and start pitching “Infrastructure Financing” to lower your cost of capital.

4. For Brokers: Deals involving Battery Energy Storage (BESS) or Solar (Grenergy, European Energy, Adani) are clearing globally. Even localized NY deals (NineDot) are getting done if they have an energy angle. This is the easiest “hook” for difficult CRE deals.

5. For Lenders: The massive multi-bank deals (e.g., $1.47B Industrial Refi involving Citi/Goldman/Morgan Stanley) are slow and complex. A single-source private credit fund that can write a $200M-$500M check can steal the “mid-tier” of this market by offering speed and certainty over pricing.

6. For Funds: The influx of massive capital ($10B+) into AI Infrastructure suggests yields will compress rapidly here. The “Alpha” is moving from owning the data center shell to financing the active equipment (GPUs/Cooling).

📈 BY THE NUMBERS: WEEK 6 MACRO

Total Capital Deployed: $25,455,305,555 (~$25.4B)

Deal Volume by League:

- CRE: 36 deals

- Growth Capital: 16 deals

- ABL: 13 deals

Most Active Lender (Overall): Ares

Ares dominated both mega-cap and mid-market brackets across multiple asset classes. In CRE led the $1.1B Bally’s casino construction deal (with King Street and TPG), and sole-financed the $450M Brooklyn geothermal multifamily refinance. In Growth Capital, Ares deployed $2.4B to Vantage Data Centers for AI infrastructure development. In ABL, Ares appeared in the $175M crane rental syndicate.

Largest Single Deal: $10B (Blackstone – AI Infrastructure, Australia)

Sector Snapshot (Cross-League Funding):

- AI/Data/Energy Infrastructure: 11 deals, $16.1B

This sector is the undisputed heavyweight champion, accounting for over half of all deployed capital. The breakdown reveals a unified thesis across international and domestic markets: AI Datacenters, GPU Infrastructure, Energy Storage (BESS), and Power Generation/Transmission - Multifamily CRE: 7 deals, $1.04B

Mix of construction completion ($128.2M Fannie Mae), lease-up/stabilization ($90M Affinius, $223.5M Invictus bridge), and affordable housing ($43.8M LA County, $34.25M Greystone). Flow heavily weighted toward stabilization capital rather than ground-up development. - Manufacturing/Industrial Services: 9 deals, $366.8M

This category captures ABL and Growth Capital deals financing operational businesses rather than real estate: Automotive/Heavy Industry, Energy Services, and Small-Ticket Working Capital

Geographic Hotspots:

- 1. Australia: $10 Billion (1 Deal)

Blackstone deployed nation-state-scale capital for the Firmus AI Factory—1.6GW of GPU/datacenter infrastructure through 2028. This single transaction equals 35% of all global capital across 66 deals, positioning Australia as a sovereign AI infrastructure hub. - New York: $1.52 Billion (7 Deals)

Led domestic markets with $431M in battery storage (28 BESS projects) plus $540M multifamily and $485M office refinancing/conversions. Energy transition infrastructure achieved parity with traditional real estate in lender appetite. - Florida: $863 Million (6 Deals)

Pure real estate play—$558.5M multifamily stabilization, $130M luxury condo development, with Invictus closing a $223.5M bridge in under 30 days. Lenders are treating stabilized Florida multifamily like liquid securities rather than illiquid real estate.

🔮 LOOKING AHEAD: WEEK 7

CRE

Look for more “Infrastructure-as-Real-Estate” deals. The $10B Australian AI project and $2.4B Denver Data Center deal indicate that “Digital Infrastructure” is effectively replacing traditional Class A Office as the new core holding for large funds.

GC:

Monitor the spread of “Energy Transition” growth capital. Deals like the $20M ethanol plant revolver and $56M Peru solar project suggest mid-market growth funds are aggressively hunting renewable energy developers who need working capital, not just project finance.

ABL: Inventory Rebuild Season

The “Refinance Wave” in ABL. Many recent deals (e.g., $175M Crane Rental, $45M Dental Services) explicitly cite “refinancing existing debt” as the primary use of proceeds. This suggests incumbent lenders are exiting, creating a prime opportunity for private credit ABL funds to capture market share.

🗳️ NOMINATE A LENDER FOR THE THE LENDER DRAFT MARCH MADNESS TOURNAMENT

Do you know a lender who is moving mountains?

We are tracking over 1,400+ lenders, but the market moves fast. If you are a lender closing deals, or a broker who just closed with a rockstar team, get them on the board.

Don’t let their deals go uncounted.

👉 CLICK HERE TO SUBMIT A DEAL NOMINATION

Help us build the most accurate bracket in commercial lending space.

The Lender Draft is tracking 1,400+ lenders competing for 96 total spots across THREE tournaments.

See full qualification standings: The Lender Draft March Madness League

Until next week, Bye-bye