📰 THIS WEEK’S HEADLINES

SPONSORED BY

📰 THE LENDER DRAFT WEEK’S RECAP

Morgan Stanley Just Went Supernova 🔥

Holy. Moly. Morgan Stanley dropped the hammer with a 99-point explosion that included a $2 BILLION construction loan for data centers in Dublin. That’s not a typo—billion with a B. They absolutely vaporized Bank OZK in what might be the most lopsided performance of the season. This is what domination looks like.

But here’s the twist: Morgan Stanley wasn’t even the only lender going off this week. The CRE bracket turned into an absolute scoring clinic, and ABL delivered some wildcard chaos.

🔥 TOP PERFORMANCES

🏆 #3 Morgan Stanley 99, #10 Bank OZK 49 (CRE)

Three deals totaling $2.38B—including that monster Dublin data center loan, a $900M Macerich REIT syndication, and a $331M CMBS acquisition. Bank OZK sat on the sidelines with zero activity. Morgan Stanley just reminded everyone why they’re a threat.

🚀 #14 ING Bank 99, #6 Bank of America 80 (Growth Cap)

ING came out of nowhere to drop 99 points on a single $394M construction loan for a 347 MWdc solar facility in Texas. As sole coordinating lead arranger, they took the whole pie. BofA posted zeros.

🔌 #6 Eldridge Capital 95, #12 USD.Ai 69 (26-point ABL beatdown)

Eldridge closed a $350M lease facility for power generation equipment (natural gas generators and modular turbines) for ProPetro Energy Solutions in Midland, TX. That’s the biggest ABL deal of the week by a mile. USD.Ai went scoreless. Eldridge vaulted 7 spots up the bracket.

💧 #1 SouthStar Capital 74, #11 First Business Bank 60 (14-point grind)

SouthStar stayed at #1 with a $750K AR facility for a Southeast building materials supplier plus an undisclosed invoice factoring deal for an AEC tech firm. First Business went quiet. SouthStar’s consistency is keeping them at the top despite modest deal sizes.

📊 THE LENDER DRAFT STANDINGS SHAKEUP

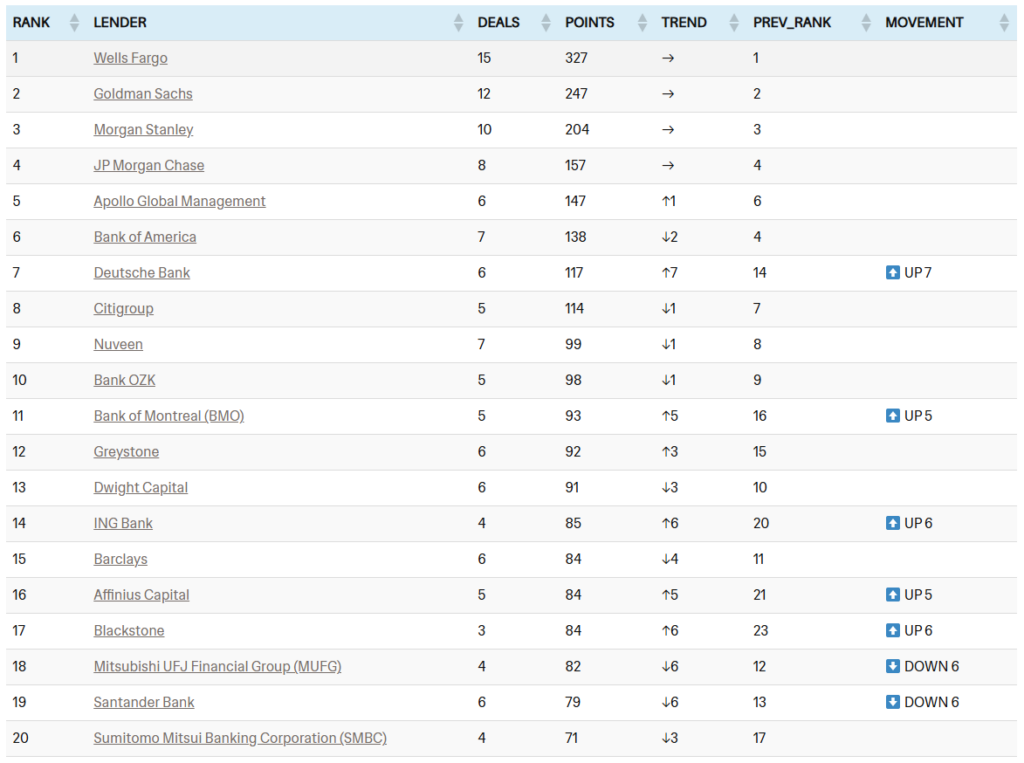

🏠 CRE LEADERBOARD

🔝 THE RISERS TO WATCH

- PGIM: ⬆️18 spots to #26 — $383M Germany retail portfolio refi = instant elevator ride

- Deutsche Bank: ⬆️ 7 spots to #7 — Macerich syndication as admin/collateral agent

- Blackstone: ⬆️ 6 spots to #17

- ING Bank: ⬆️ 6 spots to #14 — $394M Texas solar construction loan

BEST MATCHUP GAME

💰 #26 PGIM 105, #13 Dwight Capital 79 (CRE)

PGIM bested Dwight Capital by closing a $383M refinance for an 85-property retail portfolio across Germany and posted the highest single-game score of the week.

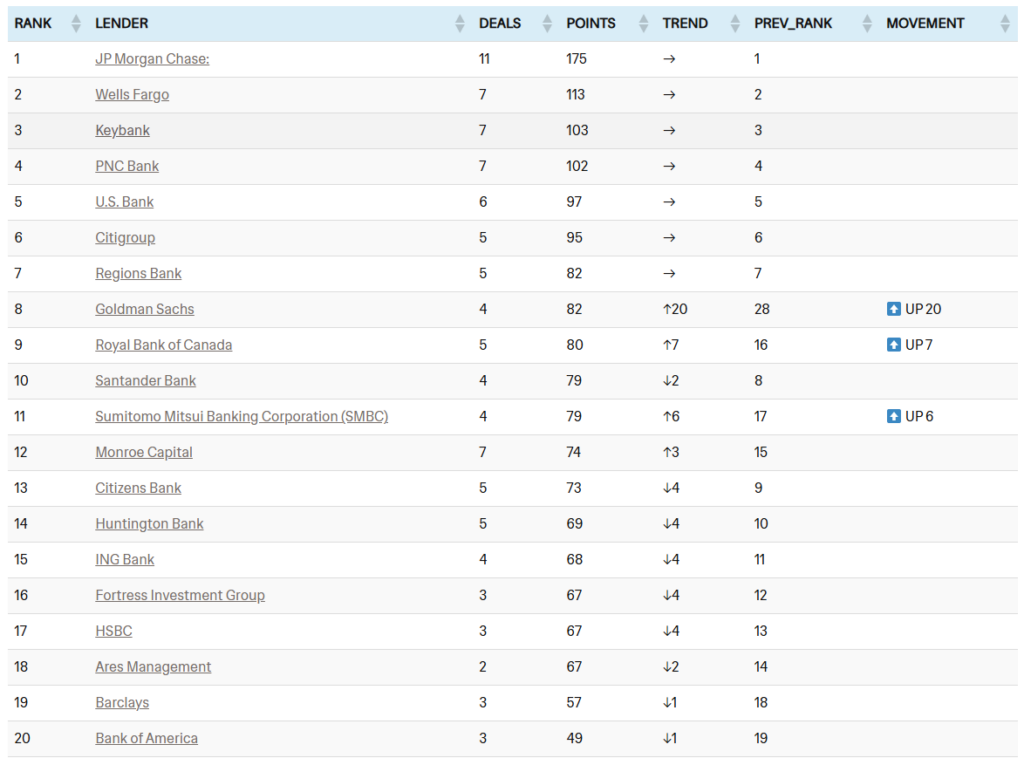

💼 GROWTH CAPITAL LEADERBOARD

🔝 THE MOVERS TO WATCH:

- Goldman Sachs: ⬆️20 spots to #8 — Macerich syndication creates MASSIVE jump

- Royal Bank of Canada: ⬆️ 7 spots to #9 — Crescent Midstream $600M facility

- SMBC: ⬆️ 6 spots to #11 — Same Crescent deal, syndication game paying off

- Monroe Capital: ⬆️ 3 spots to #12 — WGI acquisition financing

BEST MATCHUP GAME

⚡ #16 Royal Bank of Canada 101, #21 ICBC 82 (Growth Cap)

RBC outlasted ICBC by co-originating a $600M Crescent Midstream facility alongside JPM, SMBC, and others, then watched the scoreboard light up to 101. RBC jumped 7 spots and is creeping toward the top 10.

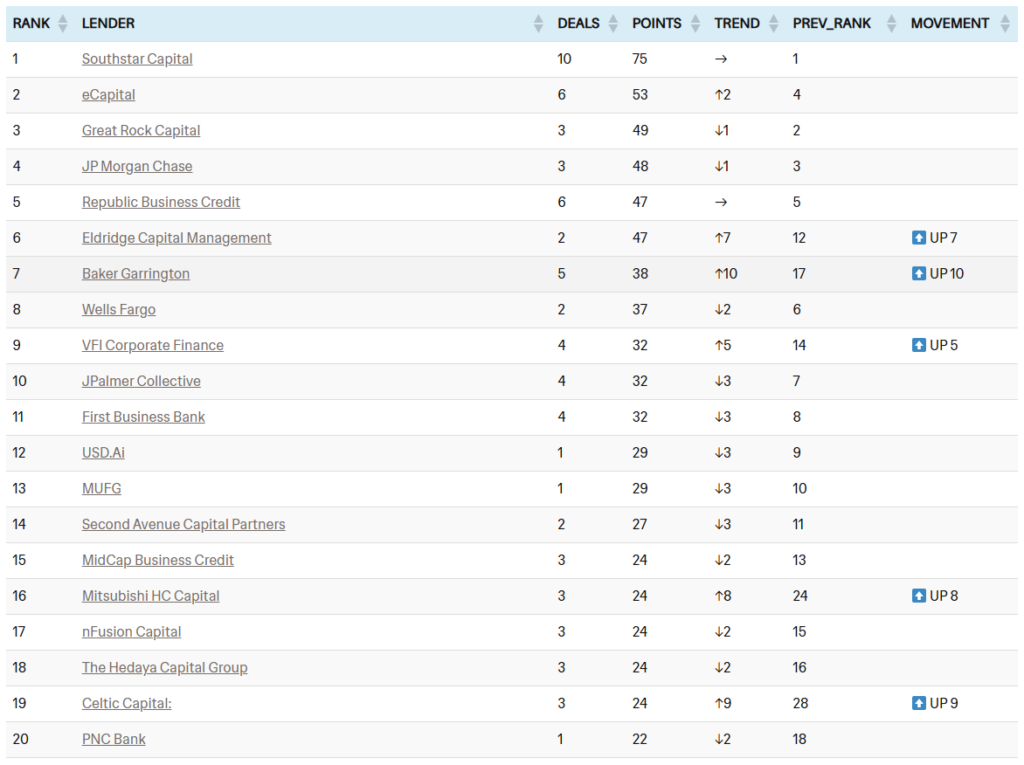

⚡ ABL LEADERBOARD

🔝 THE SIGNIFICANT RISERS TO WATCH

- Baker Garrington: ⬆️10 spots to #7 — Two oilfield factoring deals = bracket chaos

- Celtic Capital: ⬆️ 9 spots to #19 — $2.25M Pacific distributor AR line

- Mitsubishi HC Capital: ⬆️ 8 spots to #16 — Tractor dealer inventory financing

- Eldridge Capital: ⬆️ 7 spots to #6 — $350M power gen lease facility MONSTER

BEST MATCHUP GAME

🛢️ #7 Baker Garrington 94, #31 Gateway Trade Funding 78 (ABL)

Baker got a win over Gateway by deploying $4M across TWO oilfield services factoring facilities (Colorado and Tulsa-based companies) and jumped 10 spots in the ABL standings.

🏆 THE LENDER DRAFT LENDERS OF THE WEEK

COMMERCIAL REAL ESTATE

Offensive Lender of the Week: Morgan Stanley

This Week: 2 deals | 60 points

Biggest Deal: $900M Macerich Refi – Biggest deal | Multiple States (National)

Defensive Lender of the Week: Deutsche Bank

The Play: $900M revolving credit facility | Macerich REIT portfolio

Deutsche Bank served as Admin Agent AND Collateral Agent, coordinating five other banks on a $900M Macerich refi. The genius? Performance-based pricing that drops rates when the borrower hits benchmarks—incentivizing financial strength while protecting lenders. When you control the keys as admin AND collateral agent, you own the downside protection.

GROWTH CAPITAL

Offensive Lender of the Week: Goldman Sachs

This Week: 2 deals | 48 points

Biggest Deal: $600M Refi Senior Secured Loan | New Orleans, LA

Defensive Lender of the Week: Monroe Capital

The Play: Undisclosed senior credit facility | WGI acquisition (First Reserve)

Monroe financed an engineering consultancy with predictable recurring revenue from infrastructure contracts. No inventory. No commodities. Just billable hours backed by a $10B+ PE sponsor. When your borrower has sticky government clients and serious equity cushion, your downside disappears.

ASSET-BASED LENDING

Offensive Lender of the Week: Eldridge Capital Management

This Week: 1 deal | 26 points

Biggest Deal: $350M ProPetro Lease | Midland, Texas

Defensive Lender of the Week: Republic Business Credit

The Play: $2M factoring facility (accordion to $6M + $2M inventory option) | West Coast automotive parts supplier

Republic started at $2M, then built an accordion to $6M PLUS inventory lending that only unlocks IF the borrower proves performance first. Limited initial exposure with controlled upside. This is how you lend smart without taking stupid risks.

💡 WHAT THIS WEEK TELLS US

1. For Borrowers: Institutional lenders are aggressively prioritizing the “Green Premium” and Digital Infrastructure. Deals involving solar, battery storage, and AI data centers (like the $394M TX Solar or $300M Crusoe AI chip facility) are clearing the market rapidly, often with highly structured syndicates.

3. For Brokers: Grocery-anchored retail remains highly liquid. The $331.2M Blackstone portfolio acquisition in Texas and the $383.4M PGIM portfolio in Germany prove that institutional lenders will still aggressively finance retail if it is necessity-based and geographically diversified.

5. For Lenders: The proliferation of Nav Lending (e.g., $4.25M secured facility by Pacific Coast Alternatives) shows that private equity sponsors are seeking alternative liquidity without selling assets, presenting a high-yield opportunity for nimble private credit funds.

6. For Funds: Office-to-industrial conversions (like the $56.7M Doral project) and office-to-residential conversions are moving from theoretical concepts to fully funded, half-billion-dollar realities, signaling the permanent repricing and physical transformation of urban CBDs.

📈 BY THE NUMBERS: WEEK 7 MACRO

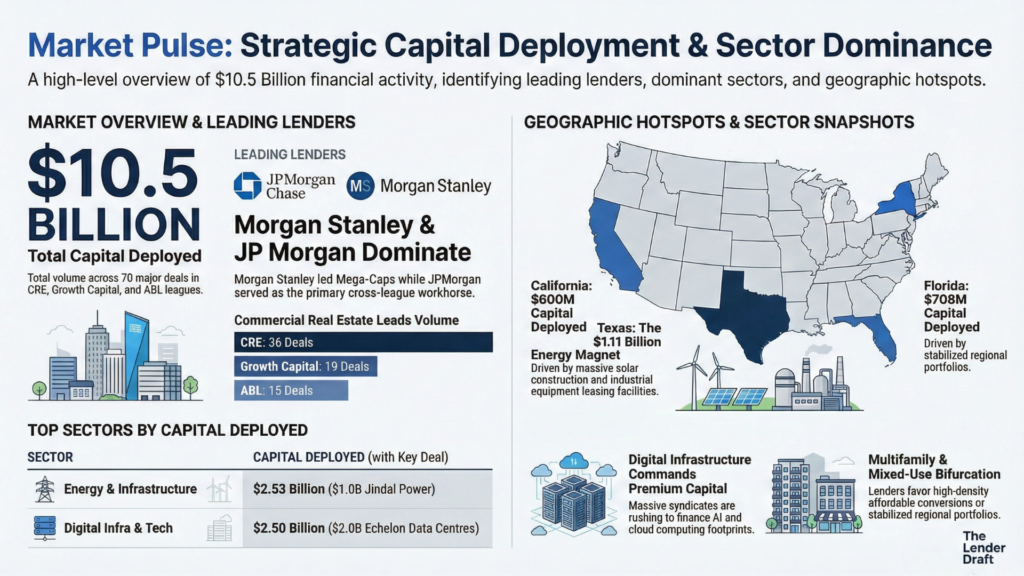

Total Capital Deployed: $10.5 Billion

Deal Volume by League:

- CRE: 36 deals

- Growth Capital: 19 deals

- ABL: 15 deals

Most Active Lender (Overall): Morgan Stanley & JP Morgan Chase

Morgan Stanley dominated the “Mega-Cap” bracket, anchoring the massive $2.0B Echelon Data Centres project internationally, originating the $331.2M Blackstone retail CMBS in Texas, and participating in the $900M Macerich syndicate. JPMorgan Chase, however, was the cross-league workhorse, co-leading the $900M Macerich facility, the $600M Crescent Midstream term loan, and a $100M growth facility for Archer Meat Snacks.

Largest Single Deal: $2.0B (Echelon Data Centres – Digital Infrastructure, Dublin, Ireland)

Sector Snapshot (Cross-League Funding)

- Energy & Infrastructure: 8 deals, $2.53 Billion

- Multifamily & Mixed-Use: 12 deals, $1.39 Billion

- Digital Infrastructure & Tech: 5 deals, $2.50 Billion

Geographic Hotspots:

- Texas: $1.11 Billion (4 Deals)

The Lone Star State remains a magnet for massive energy and industrial capital. Deal volume was driven by the $394M OCI Energy solar construction loan and the $350M ProPetro equipment lease facility. - Florida: $708 Million (7 Deals)

New York saw heavy concentration in complex, large-scale commercial real estate. Volume was anchored by the $475M RXR office-to-residential conversion in Manhattan and supported by steady middle-market multifamily financing. - California: $600 Million (9 Deals)

California attracted the widest variety of capital, leading in transaction diversity across Growth Cap, ABL, and CRE. Tech and manufacturing drove the volume, highlighted by the $300M Crusoe AI facility and the $126M Valore Holdings automotive acquisition.

🔮 LOOKING AHEAD: MARCH MADNESS TOURNAMENT

CRE

Data centers and utility-scale solar/wind are the new “Class A Office.” Expect to see massive syndications clustering around digital infrastructure pipelines and the battery storage systems required to power them.

GC:

Deep-tech and biotech (like this week’s $500M gene-editing facility) will continue to attract highly structured, milestone-based senior secured credit facilities, bridging the gap to commercialization without diluting equity in a volatile public market.

ABL:

Watch for a surge in equipment financing as industrial companies and automotive suppliers upgrade high-capacity manufacturing lines to handle newly awarded blue-chip contracts.

🗳️ NOMINATE A LENDER FOR THE THE LENDER DRAFT MARCH MADNESS TOURNAMENT

Do you know a lender who is moving mountains?

We are tracking over 1,400+ lenders, but the market moves fast. If you are a lender closing deals, or a broker who just closed with a rockstar team, get them on the board.

Don’t let their deals go uncounted.

👉 CLICK HERE TO SUBMIT A DEAL NOMINATION

Help us build the most accurate bracket in commercial lending space.

The Lender Draft is tracking 1,400+ lenders competing for 96 total spots across THREE tournaments.

See full qualification standings: The Lender Draft March Madness League

Until next week, Bye-bye