📰 THIS WEEK’S HEADLINES

SPONSORED BY

📰 THE LENDER DRAFT WEEK’S RECAP

A $2.1 BILLION data center refinance just scrambled the entire CRE bracket in one week. Five lenders co-originated the QTS deal simultaneously — meaning five teams got a stat boost on the same transaction — and the scoreboard looked like a pinball machine. Meanwhile, Wells Fargo was already sitting on a $450M CMBS close and a $215M revolving facility before QTS even hit the tape.

🔥 TOP PERFORMANCES: WHO WAS COOKING?

#1 Wells Fargo 127, #31 National Australia Bank 60 (67-point blowout)

Let’s just say Wells showed up with the entire armory. A $2.1B QTS co-origination. A $450M CMBS refinance for Nomad Tower. A $215M senior secured revolver for Orion Properties. Three deals, nearly $2.8B in total volume, and NAB didn’t close a single thing. Wells stays locked at #1 in CRE and they’re not even breathing hard.

#6 Citigroup 85, #4 PNC Bank 59 (Growth Capital) (26-point win)

In Growth Capital, Citi didn’t need volume. They needed one call. An $800M senior secured revolving credit facility refinance for Huntsman International out of Houston.

#5 Republic Business Credit 91, #30 Gateway Trade Funding 83 (8-point win)

This one went down to the wire, and Republic Business Credit earned it the hard way. A $3M invoice financing facility for a California textile manufacturer. Gateway Trade Funding went scoreless and watched Republic hold at #5 in the standings.

😱 UPSET OF THE WEEK

PGIM 75, #8 Nuveen 60 (15-point upset) — CRE

PGIM just walked into the building and handed the #8 seed their lunch. PGIM closed a $58M refinance for a mixed-use redevelopment in Quincy, MA while Nuveen — sitting pretty as one of the tournament’s top-10 teams — put up a donut. Nuveen drops two spots to #8 and suddenly the top-10 cushion doesn’t look so comfortable.

📊 THE LENDER DRAFT STANDINGS SHAKEUP

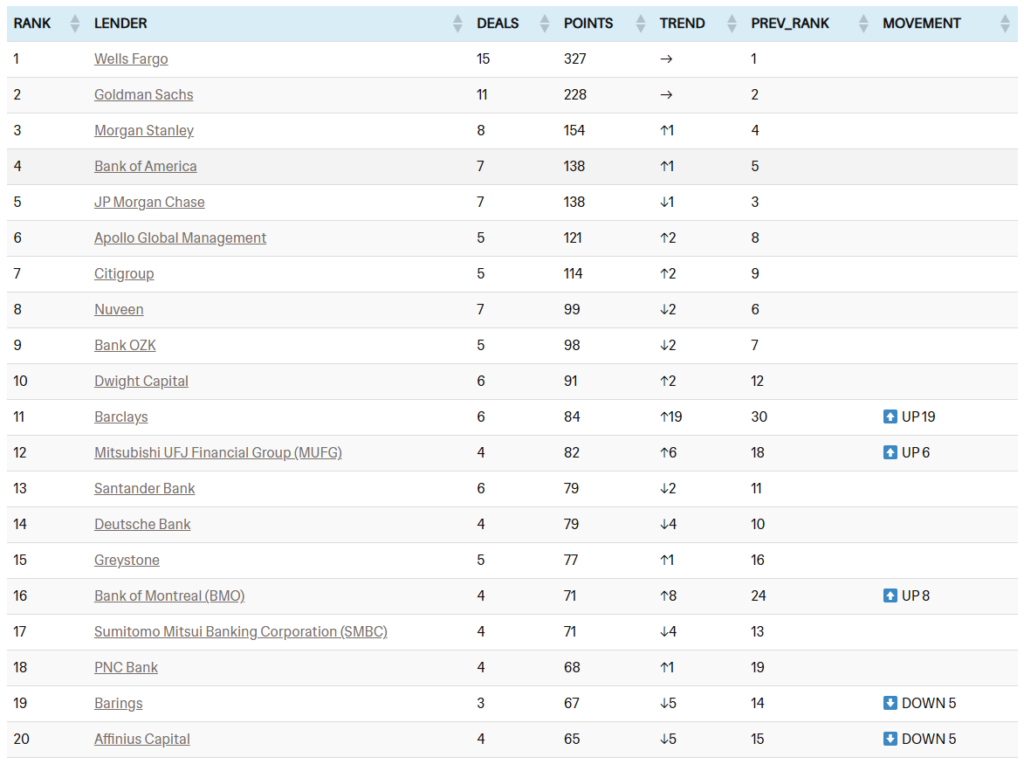

🏠 CRE LEADERBOARD

🔝 THE RISERS:

- #11 BARCLAYS ↑9 SPOTS (U.S.: 6 deals, 84 points | 3 Deals – $2.1B QTS Data Center Refi, $58M Office Refi, $17M CMBS Self-Storage Refi

- #16 BANK OF MONTREAL (BMO) ↑8 SPOTS | 4 deals, 71 points | $2.1B QTS Data Center Refi

- #12 MUFG ↑6 SPOTS (4 deals, 82 points) | $689M Lydian Energy construction deal

BEST MATCHUP GAME

#6 Apollo Global Management 98, #19 Barings 72 (26-point win)

Apollo closed a $353M senior mortgage for the Sotherly Hotels acquisition — a 10-asset Southeast portfolio — with a $45M mezz component stacked on top from Ascendant Capital Partners. Full-stack structuring, private hotel play, clean execution. Barings? Zero deals. Apollo climbs to #6 in CRE and looks like a legitimate contender. 🏨

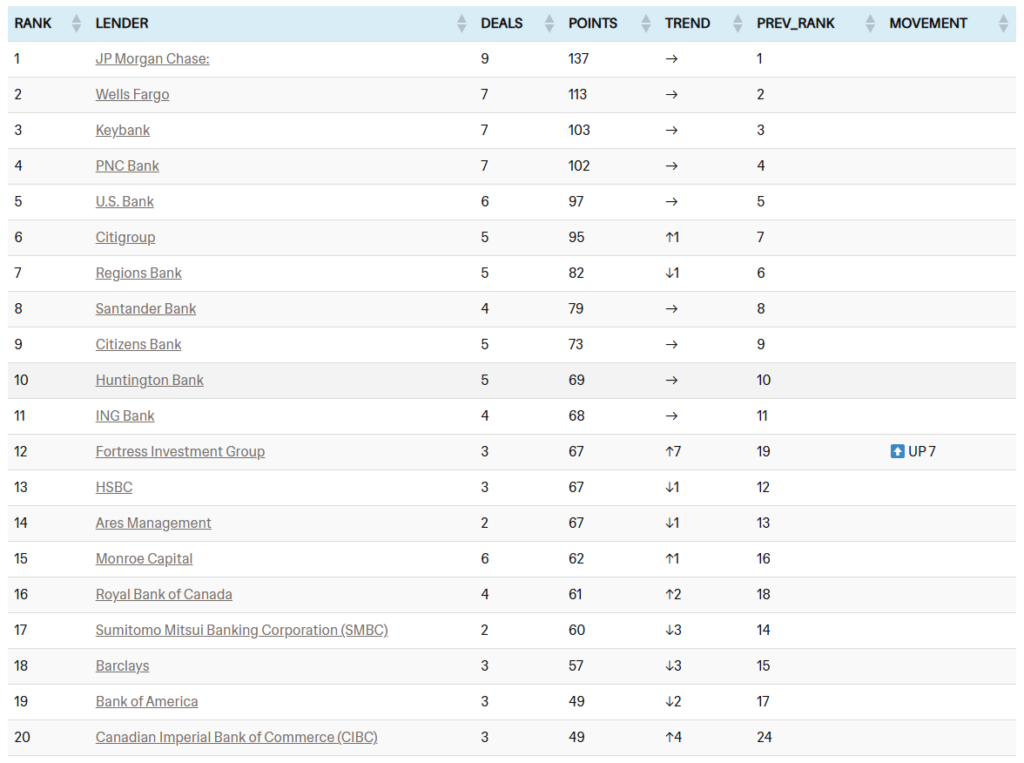

💼 GROWTH CAPITAL LEADERBOARD

🔝 THE MOVERS:

- #12 FORTRESS INVESTMENT GROUP: ↑7 SPOTS | 3 Deals, 67 Points | $112M senior secured facility for Hollywood Feed

- #20 CIBC: ↑4 SPOTS | 3 Deals, 49 Points | $50M growth capital to AlayaCare

- #16 ROYAL BANK OF CANADA: ↑2 SPOTS | $30M bilateral term loan to Western Forest Products

BEST MATCHUP GAME

#12 Fortress Investment Group 81, Barings 62 (19-point win)

While the big banks were busy syndicated $2.1B data center refinances, Fortress quietly walked into Memphis and closed a $112M senior secured credit facility for Hollywood Feed, one of the fastest-growing independent pet retail chains in the country. No syndication partners. No co-originators. Just Fortress, a borrower, and a clean deal. That’s the private credit playbook in a nutshell: find the growth story everyone else overlooked, underwrite it your way, and collect the points. Fortress sits at #12 in the Growth-Cap standings and is trending in the right direction. Don’t sleep on them.

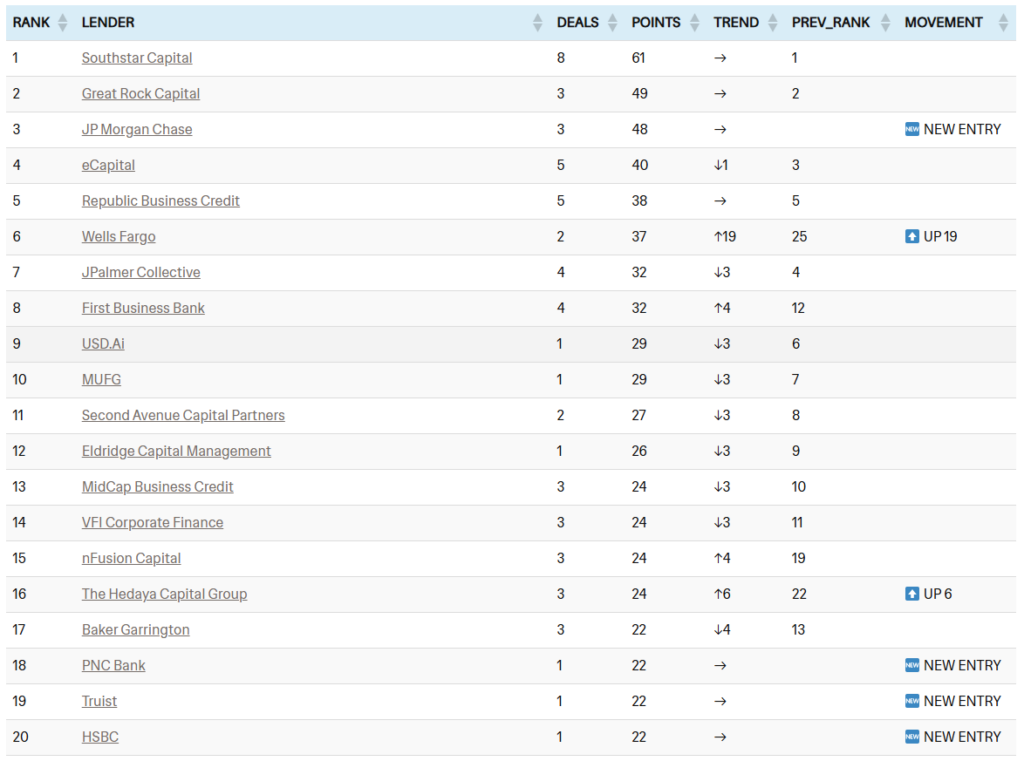

⚡ ABL LEADERBOARD

🔝 THE MOVERS:

- #6 WELLS FARGO: ↑19 SPOTS| 2 Deals, 37 Points | $1.25B Global ABL to City Electric Group

- #8 FIRST BUSINESS BANK: ↑4 SPOTS | 4 Deals, 32 Points | $2M Factoring Facility to a Virginia IT consulting services company

- #15 NFUSION CAPITAL: ↑4 SPOTS | 3 Deals, 24 Points | $5M ABL Facility to Arizona hydroponic business

- #16 THE HEDAYA CAPITAL GROUP: ↑6 SPOTS | 3 Deals, 24 Points | $8M Factoring Facility to NYC-based female-founded footwear development company

🆕 NEW ENTRY:

- JP MORGAN: 3 deals | 48 points

- TRUIST: 1 deals | 22 points

- HSBC: 1 deals | 22 points

- PNC: 1 deals | 22 points

BEST MATCHUP GAME

#15 nFusion Capital 79, #21 Comvest Credit Partners 71 (8-point win)

Here’s your sleeper story of the week. nFusion Capital, sitting at #15 in the ABL standings, closed a $5M asset-based lending facility for a hydroponic agriculture business in Arizona. Growing lettuce with borrowed money. We love it. nFusion jumped UP 4 spots to #15 on the back of one of the most creative deal structures in this week’s entire tournament. Don’t sleep on the specialty lenders. They find angles nobody else is looking at.

🏆 THE LENDER DRAFT LENDERS OF THE WEEK

COMMERCIAL REAL ESTATE

Offensive Lender of the Week: Wells Fargo

This Week: 3 deals | 63 points

Biggest Deal: 3 deals | $2.1B Industrial Refi biggest deal | Virginia, Georgia, Illinois

.

Defensive Lender of the Week: MonticelloAM

The Play: 2-tranche structure ($75M bridge loan + $5M working capital line) | 36-month term + 2x 6-month extension options | Four skilled nursing facility acquisition, Pennsylvania

GROWTH CAPITAL

Offensive Lender of the Week: Blackstone

This Week: 1 deals | 29 points

Biggest Deal: 1 deal | $600M biggest deal | Delhi, India

Defensive Lender of the Week: Lighthouse Financial Corp.

The Play: Dual-tranche structure ($7M revolving line of credit + $1.5M term loan) | Triple collateral stack (accounts receivable + inventory + machinery & equipment) | Appalachian hardwood manufacturer & distributor, Georgia

ASSET-BASED LENDING

Offensive Lender of the Week: JP Morgan

This Week: 2 deals | 30 points

Biggest Deal: 2 deals | $1.25B biggest deal | Houston, Texas

Defensive Lender of the Week: Wells Fargo

The Play: $1.25B senior secured global asset-based revolving credit facility | Borrowing base tied to eligible inventory + accounts receivable across 7 countries (US, Canada, UK, Ireland, Netherlands, Spain, Australia) | Five-lender syndicate (Wells Fargo, PNC, JPMorgan, Truist, HSBC) | City Electric Group, Houston TX

💡 WHAT THIS WEEK TELLS US

1. The QTS $2.1B refinance is the story of the week for one simple reason: it rewarded participation. Five lenders co-originated — Goldman, Citi, BofA, Morgan Stanley, Bank of Montreal, Barclays — and every single one got points on the board.

2. in ABL, we’re watching micro-lending specialists carve out territory in a completely different way — factoring facilities for female-founded footwear companies, hydroponic agriculture, IT staffing. The ABL bracket is the most creative lending environment in the tournament, and it’s not close.

3. For Borrowers: The disparity between the $2.1B digital infrastructure deals and the highly fragmented sub-$10M ABL market reveals that traditional banks are reserving balance sheet capacity for mega-cap syndications, forcing middle-market operators toward private credit and specialty finance.

4. For Brokers: Traditional commercial real estate financing is heavily skewed toward refinancing and extensions (e.g., Orion Properties’ $355M CMBS extension), indicating extremely low lender appetite for ground-up commercial office development.

5. For Lenders: The dominance of tier-1 syndicates in the $500M+ space leaves the $30M–$150M commercial construction and bridge market highly fragmented and vulnerable to agile mid-market lenders.

6. For Funds: The simultaneous funding of massive solar/battery construction ($689M) and data center refinancing ($2.1B) points to an interconnected “power and compute” super-cycle driving institutional credit markets.

📈 BY THE NUMBERS: WEEK 7 MACRO

Total Capital Deployed: $9.87 Billion

Deal Volume by League:

- CRE: 37 deals

- Growth Capital: 14 deals

- ABL: 12 deals

Most Active Lender (Overall): Wells Fargo

Wells Fargo dominated the “Mega-Cap” and syndicate bracket, appearing in the $2.1B Blackstone Data Centers refinance, leading the $1.25B City Electric global ABL, and funding major office deals ($450M Global Holdings, $215M Orion Properties).

Largest Single Deal: $2.1B (Blackstone / QTS Data Centers – Industrial/Data Centers, Virginia/Georgia/Illinois)

Sector Snapshot (Cross-League Funding):

- Multifamily CRE: 13 deals, $675.6M

The bread and butter of the CRE bracket. The flow is highly specific: it’s dominated by new construction (CLK Properties’ $115M, J&L Companies’ $110M HUD loan) and bridge acquisitions. Lenders are favoring active adult, senior housing, and affordable developments over standard middle-market value-add. - Energy & Digital Infrastructure: 10 deals, $3.93B

This sector is unequivocally the heavyweight champion of the week in terms of dollars. Between the $2.1B Blackstone Data Center refinance, the $689M Lydian Energy solar financing, and the $600M Neysa AI infrastructure deal in India, tech enablement and power infrastructure accounted for massive global syndicate volumes this week. - Office CRE: 4 deals, $1.07B

Office is staging a selective, high-dollar defense. We saw over $1.07B deployed into office assets this week. The narrative is heavily anchored by refinancing and extensions for stabilized assets, highlighted by the $450M Global Holdings tower refinance in Manhattan and Orion Properties’ $355M CMBS extension in New Jersey.

Geographic Hotspots:

- Texas: $3.3 Billion (8 Deals)

The Lone Star State takes the crown this week, driven by massive corporate asset-based lending and energy plays. The $1.25B City Electric global ABL in Houston and the $800M Huntsman chemical refinance led the state’s massive volume, supported by allocations from the $689M Lydian Energy deal. - Florida: $1.02 Billion (7 Deals)

Florida is attracting a wide variety of commercial real estate capital right now. We saw $353M go into Hospitality (Kemmons Wilson portfolio acquisition), $157M into Luxury Condo Construction (Related Ross in West Palm Beach), and $150M into Industrial portfolio acquisitions (Prospect Ridge) - California: $206 Million (9 Deals)

California narrowly trailed in total dollars but led the pack in standalone deal count (9), acting as the hub for middle-market growth capital. We saw diverse capital deployment ranging from a $50M mixed-use remediation (Comstock) to a $20M aerospace tech ABL (Drone Nerds), showcasing strong demand for specialized inventory finance.

🔮 LOOKING AHEAD: WEEK 8

CRE

Lenders are aggressively rotating capital allocations. Expect to see continued heavy deployment into data centers, renewable energy sites, and grocery-anchored suburban retail, while traditional office spaces continue to rely on short-term extensions.

GC:

The IPO window is selectively open, creating a clear exit path for mature portfolio companies. Growth capital funds are actively positioning their late-stage, cash-generative assets (particularly in AI-enabled software and specialty risk) for liquidity events.

ABL:

ABL volume is seeing a noticeable bump in the aerospace, defense, and industrial manufacturing sectors, directly fueled by global supply chain reshoring and heightened infrastructure spending.

🗳️ NOMINATE A LENDER FOR THE THE LENDER DRAFT MARCH MADNESS TOURNAMENT

Do you know a lender who is moving mountains?

We are tracking over 1,400+ lenders, but the market moves fast. If you are a lender closing deals, or a broker who just closed with a rockstar team, get them on the board.

Don’t let their deals go uncounted.

👉 CLICK HERE TO SUBMIT A DEAL NOMINATION

Help us build the most accurate bracket in commercial lending space.

The Lender Draft is tracking 1,400+ lenders competing for 96 total spots across THREE tournaments.

See full qualification standings: The Lender Draft March Madness League

Until next week, Bye-bye