📰 THIS WEEK’S HEADLINES

SPONSORED BY

Is anyone else still shivering? The first week of February has been absolutely brutal.

Here’s the thing, though: Your cash flow doesn’t care about the wind chill, and neither does Amerisource Business Capital.

I saw them close a $2.5M deal recently for a distributor in Texas, literally moving pipes and fasteners while the rest of the country was stuck on ice. That’s the kind of partner you want in your corner.

If you want a lender who executes regardless of the weather, you need to talk to Nolan. Tell him the Lender Draft sent you.

Thanks for reading The Lender Draft! Subscribe for free to receive new posts and support my work.

📰 THE LENDER DRAFT WEEK’S RECAP

February kicked off and lenders did NOT mess around. We’re talking over $7 BILLION deployed across all three leagues in one week. There were mega-syndications, double-digit bracket jumps, and enough chaos to make you spit out your coffee. If you didn’t show up with capital this week, you’re already cooked.

🔥 TOP PERFORMANCES: WHO BROUGHT THE HEAT

🏦 CRE: Citigroup 91, Wells Fargo 67

Citi straight-up embarrassed Wells. Three deals, over $2 BILLION—including a $630M multifamily monster across five states and that ridiculous $800M CMBS loan for 225 Liberty Street in NYC. Here’s the kicker: Wells was IN THE SAME SYNDICATION and still got smoked by 24 points.

💼 GC: ING Bank 97, CIBC 80

ING co-led that $1.5B Aypa Power construction warehouse facility PLUS they were mandated lead arranger on an €850M ENGIE corporate facility. Double-dip strategy = championship execution.

⚡ ABL: Eldridge Capital 86, First National Capital 60

Eldridge just redefined “big ABL” with a $375M lease facility for behind-the-meter power generation. Most ABL deals are $5M-$20M. Eldridge said “hold my beer” and closed something 20x bigger.

😱 UPSET OF THE WEEK: PNC Bank 74, Goldman Sachs 71 (CRE)

The #12 seed just took down Goldman. Goldman brought a $360M Four Seasons construction loan, but PNC countered with TWO deals: a $92.3M office-to-multifamily conversion AND a piece of that Florida Mall CMBS.

Why this matters: Deal diversity beats single-asset concentration. If you’re a borrower, lenders with flexible mandates (office conversions AND retail) move faster than single-strategy shops.

Check out full scores at thelenderdraft.com/march-madness-week-5-feb-2026-scores

📊 THE LENDER DRAFT STANDINGS SHAKEUP

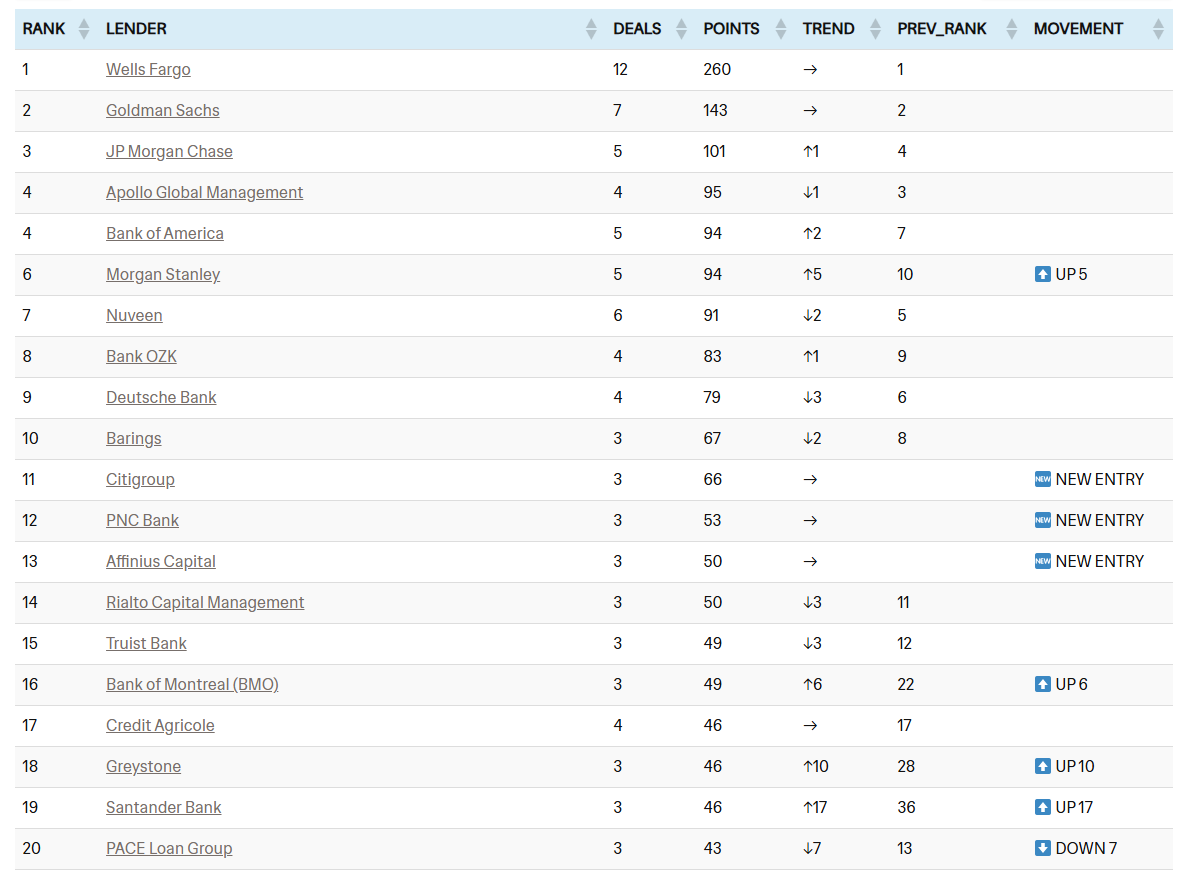

🏠 CRE LEADERBOARD

🔝 THE RISERS:

- Santander Bank (#19, UP 17 spots) 🔥 – ONE $100M Boca construction loan sent them from #36 straight into tournament position.

- Morgan Stanley (#6, UP 5 spots) – Quietly climbed with 94 points.

- Greystone (#18, UP 10 spots) – $95M Fannie Mae deal earned serious respect.

🆕 NEW ENTRIES: Citigroup (#11), PNC Bank (#12), Affinius Capital (#13) – all walked straight into the bracket.

⚠️ FALLING KNIVES: Apollo (#4), Barings (#10), Nuveen (#7) – all went scoreless and dropped. Can’t coast forever.

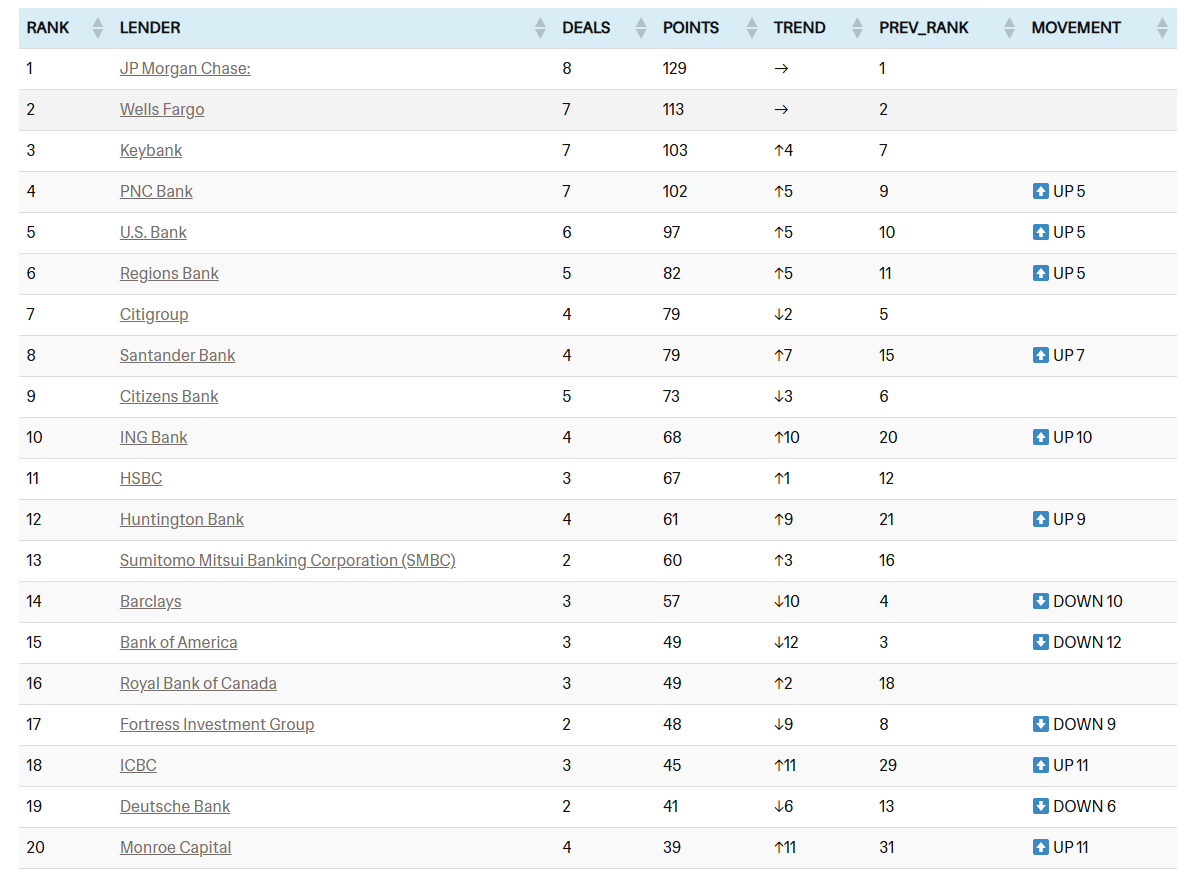

💼 GROWTH CAPITAL LEADERBOARD

🔝 THE SYNDICATION SURGE:

- Monroe Capital (#20, UP 11 spots) – #31 to #20 in ONE WEEK on that CST Academy deal.

- ING Bank (#10, UP 10 spots) – #20 to #10 in ONE WEEK on that Aypa megadeal.

- Bank of America (#15, DOWN 12 spots) – FROM #3 TO #15. Shocking collapse for a bulge bracket.

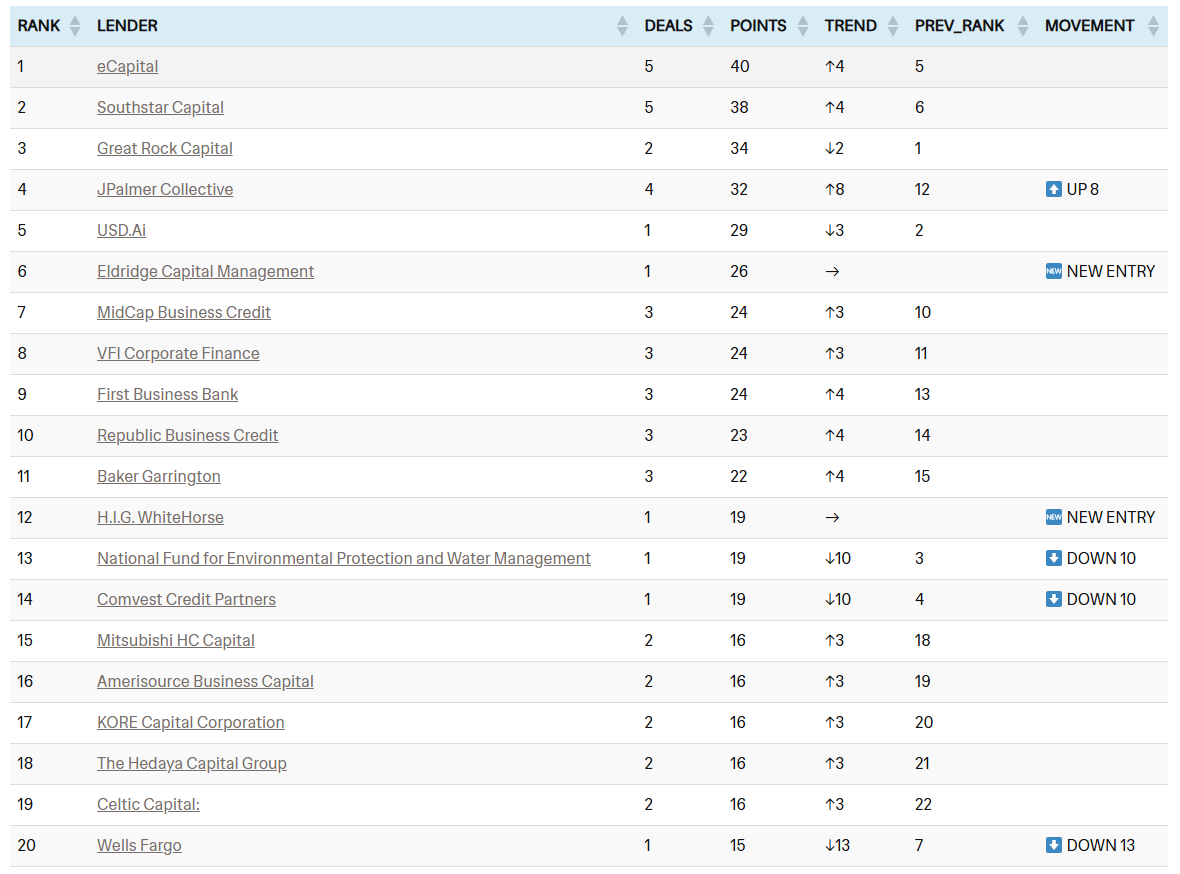

⚡ ABL LEADERBOARD

🏆 THE ELITE:

- eCapital (5 deals, 40 points) – Volume king

- SouthStar Capital (5 deals, 38 points) – Right on their heels

- JPalmer Collective (UP 8 spots) – Cinderella vibes

🆕 NEW ENTRY: Eldridge Capital (#6) – That $375M deal = instant Top 10.

⚠️ FALLING: Wells Fargo (#20, DOWN 13 spots) – From #7 to #20 on zero ABL activity. Brutal.

View full standings at thelenderdraft.com

🏆 THE LENDER DRAFT LENDERS OF THE WEEK

COMMERCIAL REAL ESTATE

Offensive Lender of the Week: Citi

This Week: 2 deals | 51 points

Biggest Deal: $800M | CMBS Refi for Brookfield Office | New York, NY

.

Defensive Lender of the Week: Bank OZK

The Play: $140.1M | Senior Construction Loan with Mezz Loan | New York, NY

GROWTH CAPITAL

Offensive Lender of the Week: PNC Bank & KeyBank

This Week: 3 deals | 45 points

Biggest Deal: $1.5B | 3-year Construction Warehouse Loan with | Austin, TX

Defensive Lender of the Week: Standard Charter Bank

The Play: 2 loans (equity investment + back leverage) | Sweden + United Kingdom

ASSET-BASED LENDING

Offensive Lender of the Week: Eldridge Capital Management

This Week: 1 deal | 26 points

Biggest Deal: $375M | Lease Facility | Austin, TX

Defensive Lender of the Week: eCapital

The Play: $17.5M ABL facility with advances against AR and inventory | Midwest US

💡 WHAT THIS WEEK TELLS US

Syndication Titles Matter More Than You Think

The Aypa Power deal showed up in EIGHT lenders’ scorecards. But CO-LEADS scored 80-97 points while PARTICIPANTS scored 64-73 points. Same deal, 15-point gap. Lead arranger titles = higher fees, better pricing, better optics.

Geography Is Alpha

UK deals dominated this week: student housing, hydraulic cylinders, Polestar equity. If you’re a U.S. borrower with European operations, you’re underutilizing your foreign assets. Most regional lenders won’t touch international receivables—but Standard Chartered, H.I.G. WhiteHorse, and Affinius will.

ONE Big ABL Deal Changes Everything

eCapital and SouthStar ground out five deals each. Then, Eldridge walks in with a $375M lease facility and jumps to #6. If your assets are hard (equipment, vehicles, energy infrastructure), there’s a lender who will go WAY bigger than you think.

📈 BY THE NUMBERS: WEEK 5 MACRO

Total Capital Deployed: $11,360,783 (~$11B)

Deal Volume by League:

- CRE: 33 deals (High volume, diverse asset classes)

- Growth Capital: 17 deals

- ABL: 9 deals

Most Active Lender (Overall): Citi (CRE) & PNC Bank (GC)

Citi dominated the “Mega-Cap” bracket, leading the syndicate for the $800M Brookfield Office refi and the $630M West Shore portfolio. PNC Bank, however, was the volume workhorse, appearing in the syndicates for the $1.5B Aypa Power deal, the $615M Orlando retail refi, and the $450M Palomar/Alpine facilities.

Largest Single Deal: $1.5B (Aypa Power – Energy Storage, Texas)

Sector Snapshot (Cross-League Funding):

- Multifamily CRE: 16 deals

The bread and butter of the CRE bracket. The flow is highly specific: it’s portfolio refinancing (West Shore’s $630M cross-state deal) and high-end construction (Goldman’s $360M Four Seasons play). Lenders are favoring stabilized portfolios or ultra-luxury developments, shying away from mid-market value-add. - Energy & Infrastructure: 7 deals

This sector is unequivocally the heavyweight champion of the week in terms of dollars. Between the $1.5B Aypa Power facility in Texas and the $1.0B ENGIE deal in France, energy infrastructure (specifically storage and wind) accounted for nearly 25% of the total global volume tracked this week. - Retail: 5 deals

Retail is staging a massive comeback. We saw over $1.4B deployed into shopping centers this week. The narrative has shifted from “distress” to “dominance,” anchored by the $615M Simon Property Group refinance in Orlando and Blackstone’s $331M acquisition of a grocery-anchored portfolio in Texas.

Geographic Hotspots:

- Texas: ~$2.33 Billion (5 Deals)

The Lone Star State takes the crown this week, driven by massive infrastructure and energy plays. The $1.5B Aypa Power deal (Growth Cap) in Austin was the single largest transaction of the week. - Florida: ~$1.95 Billion+ (7 Deals) Florida is attracting the widest variety of capital right now. We saw $615M go into Retail (Orlando Refi), $450M into Corporate Credit (Daytona Beach), and $360M into Hospitality Construction (Four Seasons Jacksonville).

- New York: ~$1.92 Billion (10 Deals) New York narrowly trailed Texas and Florida in total dollars but led the pack in deal count (9).

🔮 LOOKING AHEAD: WEEK 6

CRE: The Zero-Deal Hangover

Apollo, Nuveen, Barings, SMBC, Truist all posted donuts.. Expect a surge in bridge loan activity as sponsors scramble to refinance floating-rate debt before it matures. My prediction: at least three Top 10 lenders go scoreless in Week 6 and fall hard.

GC: The Green Wave Is Coming

Following Aypa Power’s $1.5B renewable energy success, expect mid-sized deals ($75M-$200M) in Energy Transition, Battery Storage, and EV Infrastructure as funds deploy Q1 dry powder. The sustainability premium is real.

ABL: Inventory Rebuild Season

We’re heading into the latter half of Q1 restocking for spring production. There’s a massive opportunity in the $20M-$50M segment for industrial distributors stuck between regional banks (capped at $15M) and bulge brackets (won’t look under $100M). My money’s on a non-bank lender closing a surprise $30M+ megadeal.

🗳️ NOMINATE A LENDER FOR THE THE LENDER DRAFT MARCH MADNESS TOURNAMENT

Do you know a lender who is moving mountains?

We are tracking over 1,400+ lenders, but the market moves fast. If you are a lender closing deals, or a broker who just closed with a rockstar team, get them on the board.

Don’t let their deals go uncounted.

👉 CLICK HERE TO SUBMIT A DEAL NOMINATION

Help us build the most accurate bracket in commercial lending space.

The Lender Draft is tracking 1,400+ lenders competing for 96 total spots across THREE tournaments.

See full qualification standings: The Lender Draft March Madness League

Until next week, Bye-bye