THE LENDER DRAFT: ABL POWER RANKINGS BRIEF

🏀 This Week in Growth Capital | Ending Feb 2, 2026

🔥 HOT STREAK WATCH: WHO’S GOT MOMENTUM

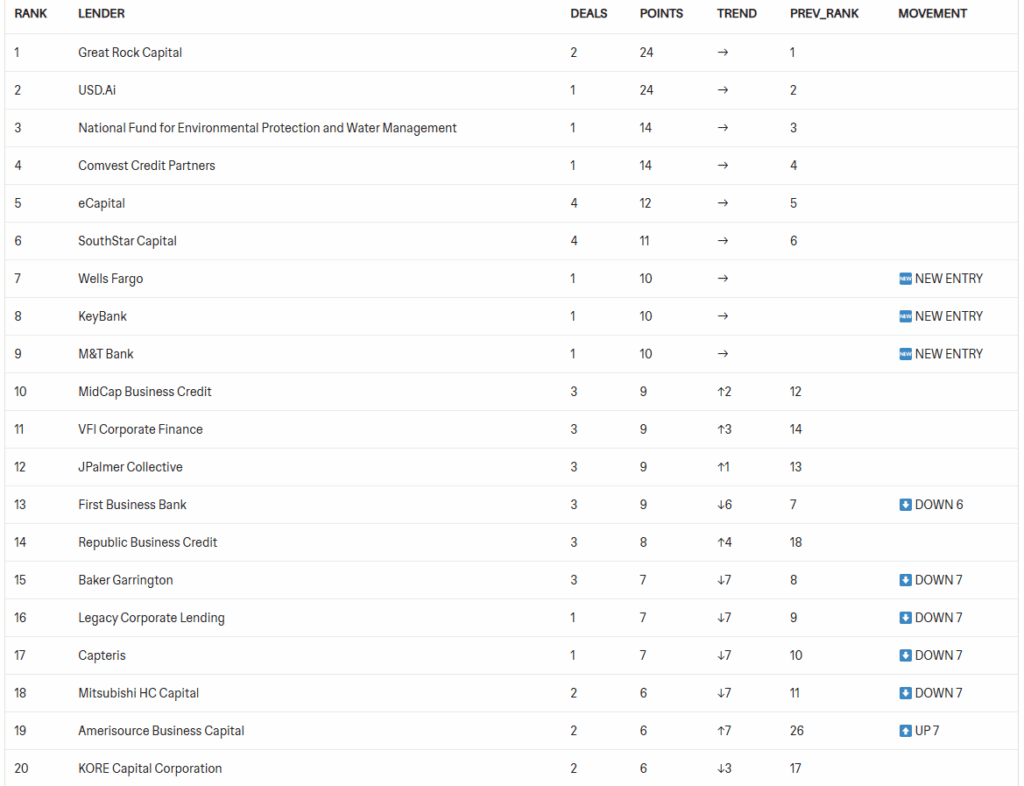

Amerisource Business Capital: #19, ↑7 (from #26)

Stats: 2 deals, 6 points, 3 pts/deal

What they funded: $2.5M A/R-only facility for a Texas distribution company doing pipes and fasteners for the energy sector

Amerisource just jumped 7 spots by grinding out smaller deals. They’re the definition of a volume player – 3 points per deal means they’re living in that $2-5M zone and doing multiples of them. Not sexy, but effective.

If you’re a borrower or broker with sub-$5M ABL deals, Amerisource is HOT right now. Like, actually hot. Call them…now

DEUTSCHE BANK: THE EUROPEAN WHO SHOWED UP TO PLAY

Republic Business Credit: #14, ↑4 (from #18)

Stats: 3 deals, 8 points, 2.67 pts/deal

What they funded: $6M ABL for a Southwest pharmaceutical manufacturer doing both branded and private-label products

Republic’s active in pharma, which is honestly a sector most ABL lenders still view like it’s radioactive (complex inventory valuation, regulatory risk, all that fun stuff). If you’ve got a healthcare supply chain play, Republic just demonstrated real appetite. Plus that $10M accordion tells you they’re willing to grow with the right borrower.

ROYAL BANK OF CANADA: QUIETLY CLIMBING

VFI Corporate Finance: #11, ↑3 (from #14)

Stats: 3 deals, 9 points, 3 pts/deal

What they funded: $6M total facility for a custom metal manufacturer ($3M sale-leaseback + $3M funding facility)

If you’re asset-rich but cash-constrained (and honestly, who isn’t these days), VFI just showed they’ll actually structure around your equipment. Most ABL lenders want clean A/R and inventory – that’s it. VFI will look at machinery, equipment, and get creative with it. That’s valuable when traditional structures just don’t fit your business.

MidCap Business Credit: #10, ↑2 (from #12)

Stats: 3 deals, 9 points, 3 pts/deal

What they funded: $12M ABL for a sponsor-owned specialty chemicals distributor (working capital revolver + equipment term loan)

f you’re a PE-backed portfolio company needing ABL, MidCap should definitely be on your list. They’re comfortable with sponsor ownership (a lot of lenders get nervous about PE involvement), and they’ll combine working capital and equipment financing in one clean structure.

JPalmer Collective: #12, ↑1 (from #13)

Stats: 3 deals, 9 points, 3 pts/deal

What they funded: $1.5M facility for Wildfang – that Portland-based menswear-inspired women’s apparel brand

JPalmer cracked the top 15 by funding what most lenders won’t even look at – apparel inventory with seasonal dynamics and long lead times. That Wildfang deal’s small ($1.5M) but super strategic for them – branded consumer products with actual retail distribution.

ROOKIE WATCH: THE NEW KIDS

|  |

Wells Fargo Capital Finance (#7), KeyBank (#8), M&T Bank (#9)

Combined stats: 1 syndicated deal, 10 each points

What they funded: $207.5M senior secured ABL facility for Revere Copper Products in Rome, NY – expansion from a previous $150M facility

Alright, so this is the actual story of the week. Three banks that weren’t even on the ABL scoreboard suddenly appear in the top 10 because they co-led this massive copper manufacturer refinancing. Wells took the lead position, KeyBank and M&T joined the party.

💡 ONE CONTRARIAN TAKE

Everyone’s celebrating the Wells Fargo/KeyBank/M&T syndication. I’m actually skeptical.

Yeah yeah, it’s a $207.5M facility. Yes, it proves large ABL syndications still work. But here’s what worries me:

It took THREE banks to do one deal. Wells Fargo, KeyBank, and M&T combined for 30 points total. That’s 10 points each. Meanwhile, USD.Ai generated 24 points from ONE deal with zero syndication partners.

What that reveals: Even “large” ABL lenders can’t hold $200M+ facilities on their own balance sheets anymore. They need to syndicate, which means:

- Longer closing timelines (coordination among three different credit committees)

- More complexity (intercreditor agreements, agent roles, fee splits, all that fun stuff)

- Less flexibility (three lenders have to agree on amendments, waivers, upsizes)

The trend I see: The future of ABL is extreme efficiency (one lender, fast decisions, $20-30M tickets) or extreme volume (10+ deals at $3-5M each, close in 3 weeks). That syndicated middle market is slow, complex, and increasingly unattractive unless you literally have no other options.

Prove me wrong: If Wells Fargo closes 3 more $100M+ ABL syndications in the next 8 weeks, I’ll totally recant this. But I think Revere Copper was opportunistic, not strategic.

NEXT WEEK’S WATCH LIST

- Amerisource Business Capital (↑7 this week): They jumped 7 spots by grinding volume in the $2-5M zone. Can they sustain this momentum or was it a one-week sprint? If they do another 2 deals next week, they’ll crack the top 15 easy.

- Wells Fargo, KeyBank, M&T Bank (all new entries): They entered with one massive syndicated deal. Will they stay active in ABL or was Revere Copper just a one-off? If Wells closes another $100M+ deal, they’ll jump straight to top 5.

- Republic Business Credit (↑4 this week): They climbed 4 spots with healthcare/pharma exposure. Are they expanding vertically into life sciences or was this just opportunistic? Watch for more healthcare deals.

- The 7-Spot Droppers (Baker Garrington, Legacy, Capteris, Mitsubishi HC): Can they stabilize or will they keep falling? If they don’t close visible deals in the next 2 weeks, they’ll probably drop another 5+ spots.

Next brief drops Monday. Until then, may your deals close fast and your spreads stay tight.

— Jude

The Lender Draft