THE LENDER DRAFT: POWER RANKINGS BRIEF

🏀 This Week in Growth Capital | Ending Feb 2, 2026

Okay, so you know how sometimes you watch a game, and you’re like “wait, who the hell is that guy and where did he come from?”

That was this week’s rankings.

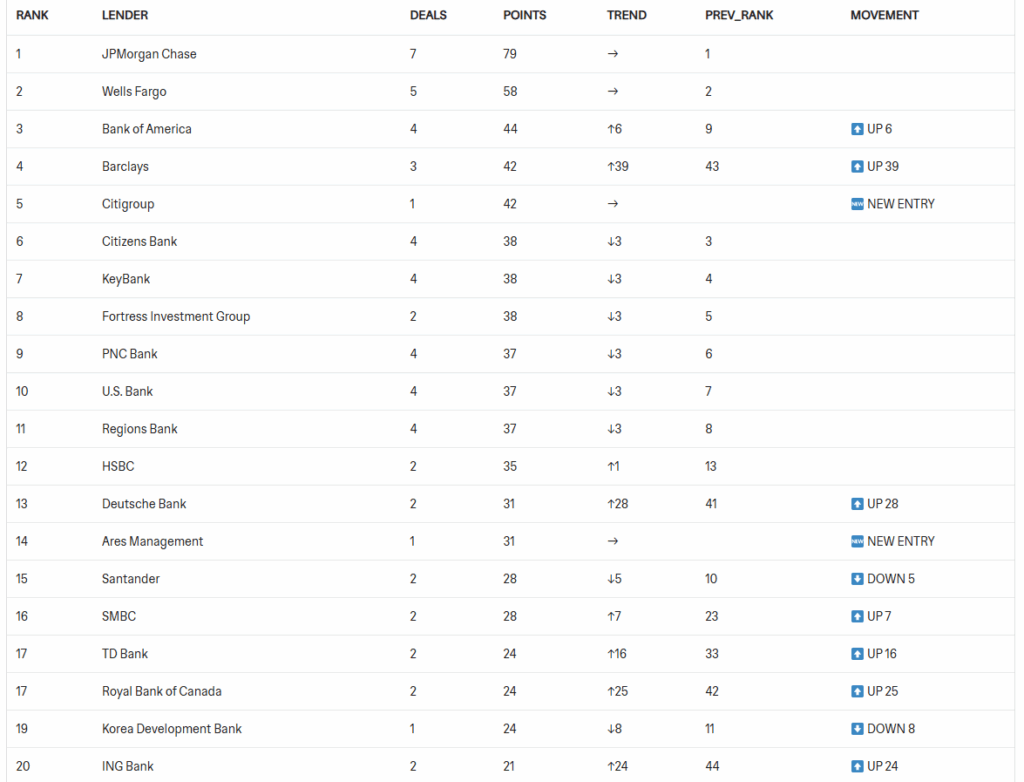

Barclays just jumped 39 spots. Not 3. Not 5. Thirty-nine. They went from literally nowhere to the starting lineup at #4 in one week. That’s like your buddy who never plays pickup suddenly showing up and dropping 40 points.

Deutsche Bank vaulted 28 spots. Royal Bank of Canada climbed 25. ING Bank jumped 24. And then Citigroup—Citigroup just casually strolled into the rankings at #5 as a NEW ENTRY with 42 points from 3 deals.

But here’s the thing: two of those deals were multi-billion-dollar international transactions. We’re talking $2.65 billion and $2.59 billion. Citi didn’t just show up to play—they showed up with a bazooka.

So what’s really happening? Two things:

One: The international banks are invading. Deutsche, RBC, ING, SMBC—they’re all pushing into US middle market like they just discovered we’re giving away free money. (Spoiler: we might be.)

Two: The mega-cap cross-border deals are where the real action is. While everyone else is grinding out $75M logistics syndications, Citi and a few others are closing billion-dollar transactions that don’t even show up on most people’s radar.

Let’s break down who’s actually winning, who’s faking it, and what the hell you should do about it.

🔥 HOT STREAK WATCH: WHO’S GOING OFF RIGHT NOW

BARCLAYS: THE GUY WHO CAME OFF THE BENCH AND DROPPED 40

Rank: #4 | Previous: #43 | Deals: 3 | Points: 42

Look, I don’t know what Barclays ate for breakfast last week, but they went from invisible to top-5 in seven days. Three deals, 42 points, averaging 14 points per transaction. For context, most lenders in this market are grinding out 10-11 points per deal. Barclays is hitting 14.

And get this, we can see they were in that massive $2.65B Cox Group deal (Spain-based energy utility acquiring Iberdrola’s Mexican business). They’re running with Citi, Deutsche, Goldman, Santander, and Scotiabank on multi-billion dollar cross-border energy transactions.

What does this actually mean? They’ve got fresh capital burning a hole in their pocket, they’re pricing aggressively to build relationships, or someone high up decided, “we’re doing big international deals now, go.”

Either way, they’re taking your calls.

What should you do about it?

If you’re borrowing: Call them. Like, today. They’re at #4 and they NEED to stay there. But here’s the thing, based on what they actually funded, they’re hunting $100M+ deals with international angles. If you’ve got cross-border exposure or big-ticket growth capital needs, they’re your new best friend.

If you’re a broker: They need deal flow to sustain this. Bring them your A-paper with scale. They just did a $2.65B deal, they’re not afraid of size.

If you’re competing with them: Watch their next three deals like a hawk. A 39-spot jump on international mega-deals tells you they’re building a cross-border growth capital practice.

DEUTSCHE BANK: THE EUROPEAN WHO SHOWED UP TO PLAY

Rank: #13 | Previous: #41 | Deals: 2 | Points: 31

Deutsche climbed 28 spots with just 2 deals at 15.5 points each. And we can see exactly what they did:

$365M Gerald Group (Swiss metals/minerals commodity trader) – massive international syndication

$2.65B Cox Group (with Citi, Barclays, Goldman, etc.) – Spain-to-Mexico energy M&A financing

You see the pattern? Cross-border, commodity-linked, energy, complex structures. They’re not here for your vanilla $50M SaaS growth capital deal.

What should you do about it?

If you’re borrowing: Got international revenue? Commodity exposure? Energy sector? Cross-border M&A? Call Deutsche. They just funded a Swiss metals trader and a Spain-Mexico energy deal in the same week.

If you’re a broker: Don’t waste their time with straightforward, domestic-only deals. Bring them the stuff with 3+ countries involved and watch them light up.

ROYAL BANK OF CANADA: QUIETLY CLIMBING

Rank: #17 (tied) | Previous: #42 | Deals: 2 | Points: 24

RBC jumped 25 spots, and here’s the thing—we can see exactly how they did it:

$375M First Industrial logistics REIT deal (with Wells, JPM, BofA, etc.)

$2.588B Exchange Income Corp (Canadian aerospace/aviation/manufacturing company) – they’re in the syndicate

Translation: RBC is playing both sides. They’re following Wells Fargo into safe US logistics deals while also participating in massive Canadian growth capital transactions. Smart.

What should you do about it?

If you’re borrowing logistics/supply chain/industrial RE: RBC just announced they’re building a book in your sector. Call them before they fill up.

If you’re Canadian or have Canadian operations: RBC is obviously a call for you, but this $2.588B Exchange Income deal shows they’re active in aerospace/aviation too.

ING BANK: THE VOLUME GRINDER

Rank: #20 | Previous: #44 | Deals: 2 | Points: 21

ING vaulted 24 spots with 2 deals at 10.5 points each, they’re playing in the $60-80M range. Not hunting elephants, just grinding volume in the middle of the fairway.

What should you do about it?

$50-100M growth capital in proven sectors? ING is your call. They’re building a US book and they’re not going to nickel-and-dime you on terms.

HSBC: DON’T SLEEP ON THE QUIET ONE

Rank: #12 | Previous: #13 | Deals: 2 | Points: 35

HSBC only moved up one spot, so you might skip over them. Don’t.

Check that efficiency: 17.5 points per deal. That’s the highest efficiency in the top 15 outside of Ares. Two deals, 35 points—they’re hunting $125M+ transactions.

What this tells you: HSBC isn’t playing the volume game. They’re waiting for the right pitch and then swinging for the fences.

What should you do about it?

If you’ve got a $100M+ deal: Call them immediately. They’re not buried in pipeline so they’ll move fast.

👑 DEFENDING THE THRONE: THE TOP 3

#1 JPMORGAN CHASE: STILL THE CHAMP (BUT FOR HOW LONG?)

Rank: #1 | Previous: #1 | Deals: 7 | Points: 79

JPMorgan’s holding #1 with 7 deals and 79 points, but here’s the thing—that arrow pointing right (→ flat) is telling. They’re not expanding. They’re defending.

We can see they were in:

The $375M First Industrial logistics deal

The $2.588B Exchange Income Corp Canadian deal

So they’re playing both the US middle market syndication game AND the mega-cap international game. That’s how you stay #1, diversification.

Efficiency check: 11.29 points per deal puts them in the “balanced player” zone. They’re everywhere, picking up points through sheer volume and strategic participation.

What does this mean for you?

Borrowers: JPMorgan should STILL be your first call for $75M+ growth capital. Being #1 with a flat trend doesn’t mean they’re pulling back—it means they’re not desperate. You’ll get professional execution, clean docs, reliable closes… but you won’t see aggressive pricing.

Brokers: Use JPM as your anchor but shop aggressively around them. They need to defend that #1 spot but they’re not hungry enough to overpay.

Competing lenders: JPM’s maintaining through diversification. They’re in everything from $150M middle market deals to $2.5B international transactions. Hard to compete with that range.

#2 WELLS FARGO: THE LOGISTICS KINGPIN

Rank: #2 | Previous: #2 | Deals: 5 | Points: 58

Wells holds #2 with 5 deals and 58 points, and we can see EXACTLY what they’re doing:

The deals:

LED the $425M First Industrial Realty Trust unsecured term loan (SOFR + 85 bps!)

Participated in the $375M First Industrial expansion

LED the $125M Targeted Lending Co. equipment finance facility

Participated in the $2.588B Exchange Income Corp deal

You see the pattern? Logistics. Supply chain. Equipment finance. Industrial real estate. Aerospace/aviation.

Wells isn’t chasing shiny objects. They’re grinding in defensive sectors with proven cash flows and tangible collateral.

What does this mean for you?

Borrowers in logistics/supply chain/industrial RE/aerospace: Wells is literally your only first call. They just funded TWO massive First Industrial refinancings in one week at SOFR + 85 bps for UNSECURED paper. They own this sector.

Brokers: If it’s logistics or supply chain, Wells is the safe bet. They’ll price competitively and close fast.

#3 BANK OF AMERICA: THE “YES BANK”

Rank: #3 | Previous: #9 | Deals: 4 | Points: 44

BofA climbed 6 spots to crack the top 3, and here’s how they did it: they said yes to everything.

We see them in:

BOTH First Industrial deals and $2.588B Exchange Income Corp deal

That’s their whole strategy—show up for every major syndication, accumulate points through participation, don’t try to be a hero.

What does this mean for you?

Borrowers: BofA is a phenomenal #2 or #3 lender in your syndicate. They’ll follow strong lead arrangers, they’ve got the balance sheet to provide scale, and they’ll close fast. Just don’t expect structural creativity. Expect reliability.

ROOKIE WATCH: THE NEW KIDS

CITIGROUP: THE INTERNATIONAL MEGA-DEAL MACHINE

Rank: #5 | Deals: 3 | Points: 42

Okay so let me tell you what Citi actually did, because this is wild:

Deal 1: $150M Eve Air Mobility (eVTOL aircraft developer in Florida)

Syndicate: Itaú, Banco do Brasil, Citibank, MUFG

Purpose: Advance eVTOL development, certification, strategic roadmap through 2028

Translation: Electric air taxis. Citi’s betting on urban air mobility.

Deal 2: $2.65 BILLION Cox Group (Spain-based energy utility)

Syndicate: Citi, Barclays, BBVA, Deutsche, Goldman, Santander, Scotiabank

Purpose: Acquire Iberdrola’s Mexican business ($4.2B valuation, 2.6 GW of power generation)

Translation: Massive cross-border energy M&A financing. This is where most of Citi’s points came from.

Deal 3: $2.588 BILLION Exchange Income Corp (Canadian aerospace/aviation/manufacturing)

Massive Canadian syndication with National Bank, CIBC, TD, RBC, Scotia, BMO, Wells, BofA, JPM, etc.

Purpose: Fund M&A, Air Canada contract expansion, organic growth

Translation: Another multi-billion dollar international growth capital facility.

So here’s what’s actually happening:

Citi entered the rankings at #5 with 3 deals totaling 42 points (14 pts/deal efficiency). But TWO of those deals are multi-billion dollar international transactions. They’re not playing the middle market game—they’re playing the mega-cap cross-border game.

What does this tell you about Citi’s strategy?

They’re focused on international deals. All three deals have cross-border elements (Brazil/US, Spain/Mexico, Canada/multi-country).

They’re betting on specific sectors: Energy infrastructure ($2.65B), aerospace/aviation ($2.588B), and future mobility ($150M eVTOL).

They run with the big dogs. Look at who they’re syndicating with: Goldman, Deutsche, Barclays, Santander in Spain. National Bank, CIBC, TD, RBC in Canada. These aren’t middle market syndicates—these are bulge bracket cross-border deals.

What should you do about it?

If your growth capital need is $100M+ with international exposure: Call Citigroup. They just did three deals ranging from $150M to $2.65B, all with cross-border angles.

If you’re in energy infrastructure, aerospace/aviation, or future mobility: Citi’s clearly betting on these sectors. The $150M eVTOL deal is especially interesting—shows they’re willing to go into emerging tech with the right story.

If you’re purely domestic middle market: Probably not your call. Citi’s playing a different game.

Brokers: Bring Citi your largest, cleanest deals with international angles. They’re selective but they close big.

ARES MANAGEMENT: THE OTHER ELEPHANT IN THE ROOM

Rank: #14 | Deals: 1 | Points: 31

Ares debuts at #14 with 1 deal worth 31 points (31.0 pts/deal). This is probably a $200-250M growth capital deal.

What does this mean?

Ares is playing the same selective game—large-ticket, high-conviction. They’re direct lenders with permanent capital, so they can be patient and picky.

What should you do about it?

$150M+ growth capital in sponsor-backed platforms? Ares brings patient capital and strategic relationships.

NEXT WEEK’S WATCH LIST

- Barclays → Can they hold #4 or was this a one-week spike on the Cox Group deal?

- Citigroup → Will they close more international mega-deals or was this week an outlier?

- Deutsche Bank → They’re clearly building a cross-border energy/commodity practice. Watch for more.

- Santander → They were in the $2.65B deal and still dropped 5 spots. That’s concerning. Do they stabilize or keep falling?

- Wells Fargo → Can they hold #2 against the international mega-deal machines?

Next brief drops Monday. Until then, may your deals close fast and your spreads stay tight.

— Jude

The Lender Draft